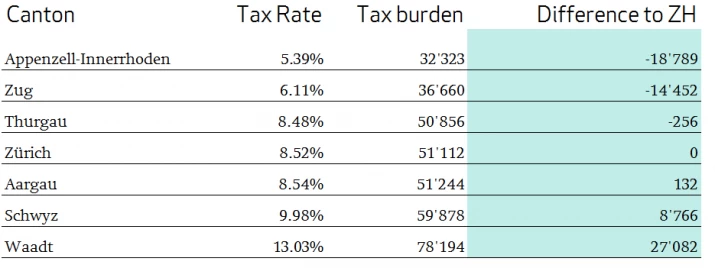

Zurich is in mid-table for smaller withdrawals. For very high lump-sum withdrawals, the tax burden in the canton remains considerable in a national comparison. The municipal tax rates must also be taken into consideration, however. The city of Zurich rate used for the calculation is relatively expensive. In the municipality of Kilchberg, the tax rate on a withdrawal of CHF 1,000,000 would be only 9.48% overall, due to the lower municipal taxes.

Conclusion

With the amendment of § 37 of the Zurich tax code, the canton will become more attractive for the withdrawal of lump-sum benefits, especially as many payments (e.g. also advance withdrawals to finance residential property) are likely to be within the now relieved range.

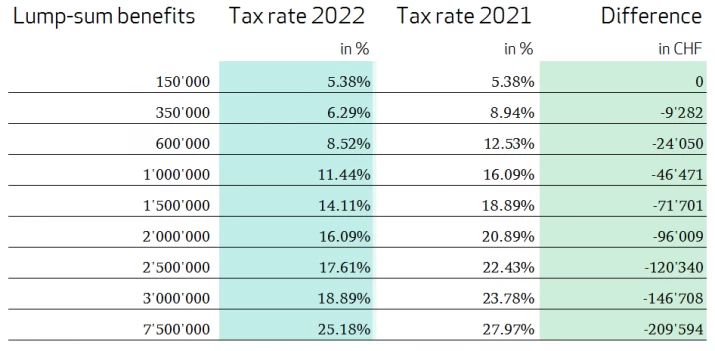

Since the tax burden is being reduced on mid-range lump-sum benefits in particular, it is important to ensure that withdrawals are staggered instead of making one high withdrawal in one year. This applies throughout Switzerland and is likely to be a well-known fact. Due to the new regulation in the canton of Zurich, however, this aspect seems to us to be somewhat more important here. Another point is the time component. If a lump-sum benefit can be drawn both in 2021 and in the years thereafter, it should not be withdrawn until 2022 – in which case the new § 37 of the Zurich tax code will apply. A change of residence is unlikely to be necessary in most cases, especially since in many constellations the payments were also deductible in Zurich. However, if you are planning to spend your retirement somewhere else in Switzerland – or even abroad – anyway, it is advisable to check exactly when a withdrawal makes sense.